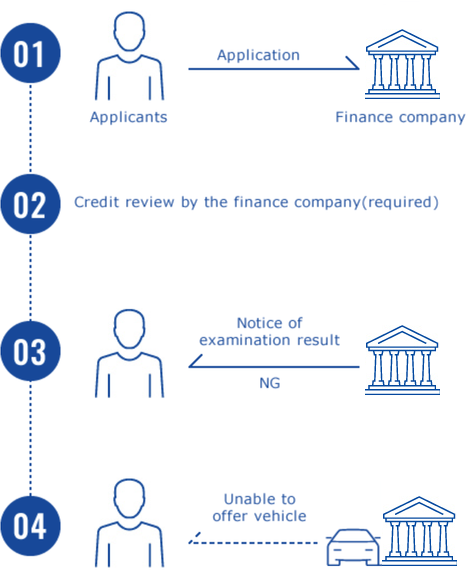

According to the 2017 Findex Report, around 1.4 billion adults remain unbanked. Without a credit history, it is challenging for the unbanked to apply for loans and pass loan screenings. Further obstacles, such as lack of collateral, play a role in limiting financial access to underserved communities.

Left with minimal options, the unbanked who use a vehicle as a mean for work often pay to rent the vehicle, and the high rental fees take a significant percentage of their income without allowing them to build a credit history or own the vehicle.

In a conventional thinking, creditworthiness is how a lender determines the applicant’s ability to repay the loan. In following this logic, many workers who do not have creditworthiness but can pay the loan are left out of the picture.

® Registered trademarks GMS is registered trademark of Global Mobility Service Inc.